Think you’ve got the perfect retirement plan? Think again. We’ve found many new retirees end up modifying their plan after they retire. No plan is perfect, so investors need to remain open to considering alternatives. We’re going to cover:

- The reality of drawing Social Security benefits.

- How to build a portfolio for retirement.

- Which common activities sabotage future retirement plans.

Social Security Benefits

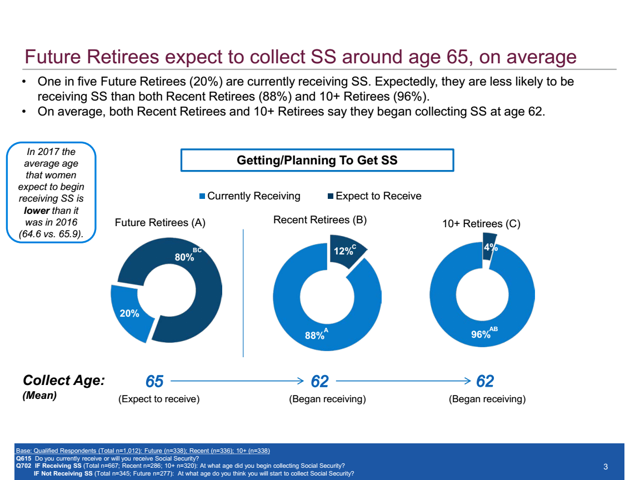

Many future retirees expect to begin drawing Social Security around 65. Like most beliefs about retirement, the actual results tell a different story.

Those who are already retired had an average starting age of 62:

Source: Nationwide

It would be reasonable to conclude that many people begin drawing Social Security earlier than they intended to.

If the investor is terminated for any reason within 1 or 2 years of their retirement date, they may not wish to endure a job hunt. Even if they found a new position, they would still need to get through the orientation. Workers go through that process every day, but most are planning to continue working for many years.

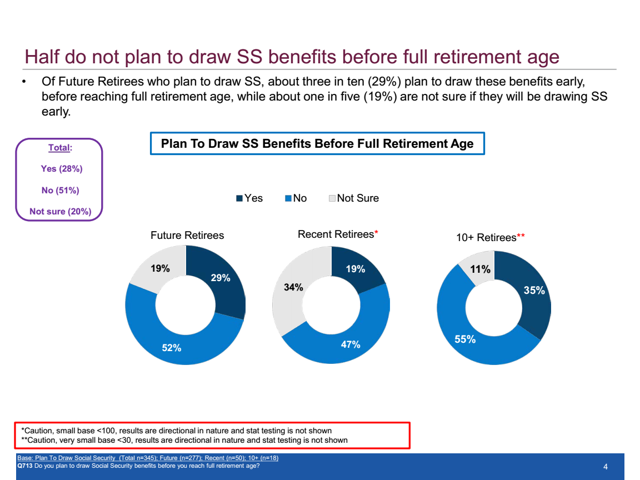

Waiting on Social Security

However, the retirees who are not drawing Social Security were not included in the averages. If we factor in those people, the story looks a little different. 19% of new retirees are still planning to wait for full retirement age. That"s down quite a bit from the 29% of future retirees who state that goal.

Source: Nationwide

It is worth pointing out that the sample sizes were pretty small. Perhaps the numbers would change with larger sample sizes. We suspect the trend would still hold true, but the precise figures might change a little.

Are Retirees Happy?

Most retirees end up filing for Social Security benefits before their "full retirement age". There is nothing inherently wrong with taking Social Security early. Yet, it’s important for investors to plan ahead.

Make the best choice for you.

While 15% to 16% regret drawing at a younger age, 73% to 78% state they are happy with their choice.

What Steps Should You Do?

Let"s start with a quick look at a few things investors should do:

- Maximize contributions to tax-advantaged accounts.

- Purchase strong companies with excellent balance sheets (eliminating some of the gambling behavior that is far too common).

- Purchase shares in low-fee index funds if you don"t like to manage your investments.

There are some areas where low-fee index funds provide the best possible exposure. For instance, investors looking for diversified bond exposure should look to index funds. Most of these funds will provide a yield that is fairly low but also steady.

We"re not a fan of moving into junk bonds. Investors assume that the yield will continue, but completely underestimate the risk of a recession sending several of the companies into bankruptcy.

We’ll start with looking at ways to build individual stock portfolios, and then we’ll cover the index fund options.

Building a Stock Portfolio for Retirement

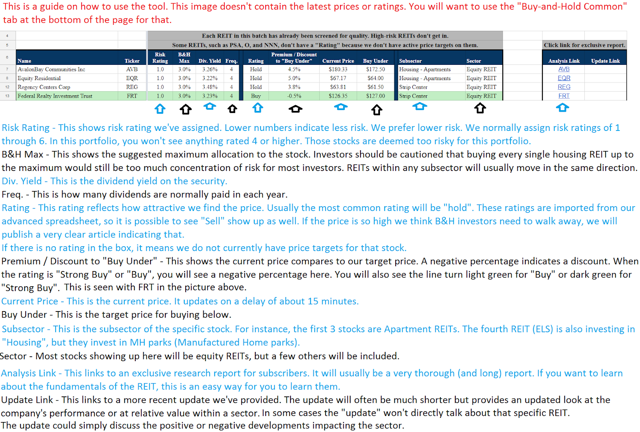

We"ve prepared a handful of articles on how to retire in your 60s with a defensive portfolio. We even built a tool for identifying lower-risk REITs to help investors. We call it the "Safe Income Portfolio" and provide it to subscribers of The REIT Forum. It can be accessed with just a couple of clicks on our service. We fill it with REIT shares that have a risk rating lower than 4. Our risk rating scale runs from 1 to 5 with 1 being the lowest. This portfolio creates an easy way for investors to filter out the lower quality REITs. We don"t suggest that investors need to purchase every share in the portfolio. Instead, investors should think of it as a buffet where we"ve carefully evaluated each item.

For instance, it includes AvalonBay (AVB), Equity Residential (EQR), Regency Centers Corp. (REG), and Federal Realty Investment Trust (FRT). Those examples include two apartment REITs and two strip center REITs, but there are several other REITs that also qualify.

The chart below demonstrates how it works and includes 4 of the shares with a risk rating of 1:

We also own positions in several shares that are included in the portfolio. We believe this is a great time to focus on buying quality REITs and preferred shares.

Buying Common Shares

The traditional way to build a portfolio is to focus on common shares. We suggest that investors look to invest in larger companies with a healthy amount of research available. Beyond the REITs we cover, these are several other highly-covered companies on Seeking Alpha:

Consumer Staples | Healthcare | Consumer Discretionary | Technology & Others | ||||||||

Target | (TGT) | 3.19% | Gilead Sciences | (GILD) | 3.96% | General Motors | (GM) | 4.10% | Apple | (AAPL) | 1.55% |

Altria Group | (MO) | 5.64% | Merck & Co. Inc. | (MRK) | 2.66% | Ford Motor Company | (F) | 6.84% | AT&T Inc. | (T) | 6.58% |

Walmart | (WMT) | 2.18% | Eli Lilly & Co. | (LLY) | 2.00% | Disney | (DIS) | 1.59% | Verizon | (VZ) | 4.08% |

Philip Morris | (PM) | 5.22% | Johnson & Johnson | (JNJ) | 2.59% | McDonald"s | (MCD) | 2.45% | Intel Corporation | (INTC) | 2.37% |

High Dividend ETFs | Bond ETFs | Preferred share ETFs | Sector ETFs | ||||||||

Vanguard Dividend Appreciation ETF | (VIG) | 1.91% | iShares Core US Aggregate Bond ETF | (AGG) | 2.72% | iShares US Preferred Stock ETF | (PFF) | 6.01% | Vanguard Real Estate ETF | (VNQ) | 4.57% |

Vanguard High Dividend Yield ETF | (VYM) | 3.07% | Vanguard Total Bond Market ETF | (BND) | 2.79% | Invesco Preferred Portfolio ETF | (PGX) | 5.74% | Vanguard Consumer Staples ETF | (VDC) | 2.61% |

Schwab US Dividend Equity ETF | (SCHD) | 2.84% | Vanguard Short-Term Bond ETF | (BSV) | 1.98% | First Trust Preferred Securities and Income ETF | (FPE) | 5.83% | Invesco QQQ ETF | (QQQ) | 1.00% |

No comments:

Post a Comment