Facebook (FB) continues to defy the market expectations by growing revenues and earnings, and buying back lots of stock. Nonetheless, it appears that extreme pessimism has led the stock to trade at mind-boggling valuations. I expect the stock to report a modest 2019 before resuming its usual exemplary performance in 2020. FB is too cheap to ignore and continues to be my highest-conviction buy.

Blood In The Streets

FB has been a terrible stock to own this year. The current environment, however, suggests that this has more to do with extreme pessimism rather than objective logic. The company"s recent earnings had a lot to be optimistic about.

Revenues grew 33% YOY, and management guided for the growth to drop at mid- to high-single digit rates next quarter as well. This suggests a Q4 revenue growth rate in the 24-27% range, which looks to be much better than many projections, and that called for growth to slow down to 20%. I also liked that FB used basically 100% of free cash flows on share repurchases. While the company has only recently begun buying back shares since 2017, the management team is showing tremendous maturity in returning cash to shareholders, especially when prices keep going lower.

There were indeed some disappointing notes. Operating margins dropped from 50% to 42%, which was a less-than-“gradual” decline as one would have expected when management said that operating margins would trend toward the mid-30s “long term.”

Management did indicate that the largest changes to the company"s margin structure would happen in 2019. I caution that 2019 may appear to be a mixed bag financially; I expect revenues to continue to grow, but the bottom line to be pressured due to expense growth. 2019 looks to be a crucial year in which FB intends to front-load significant amounts of capital expenditure and set the foundation in place to make sure that it never allows the data privacy issues that surfaced in the past two years to ever happen again. We will look at how this impacts the numbers in just a moment. I appreciate that the company is able to complement this forward thinking with share repurchases which help to boost shareholder value in the near term.

Nonetheless, there appears to be blood in the streets now. Countless articles like this one are released almost every week implying that morale is low, and as a result, FB employees are leaving in aggregate. This just does not add up, as while I can believe that these are not necessarily the best of times due to the poor stock price action, FB employees are treated to free food and work at a Disneyland-like campus. Even more articles try to imply that FB is seeing massive user backlash and seeing users deleting their accounts en masse.

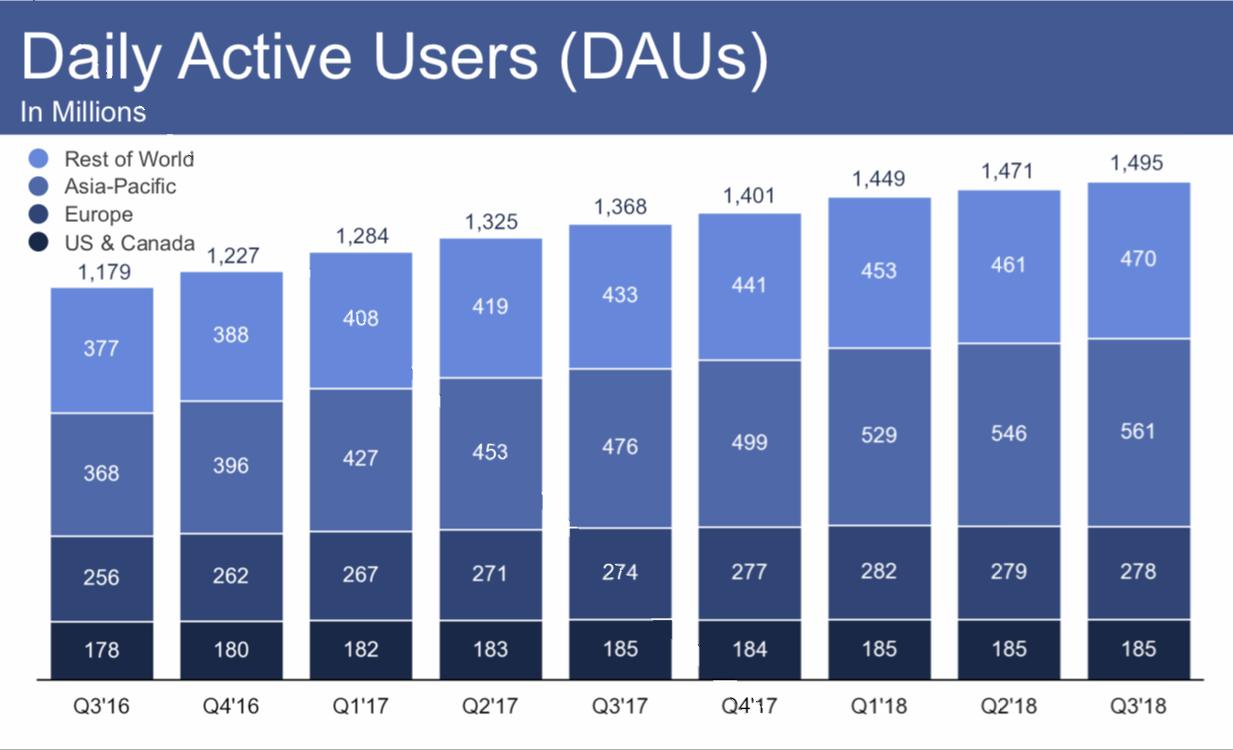

The company proved these conjectures wildly off base when it showed very minimal declines in Europe and North America plus modest user growth overall:

(Source: 2018 Q3 Presentation)

I continue to find FB to be that rare combination of a company capable of compounding earnings at double-digit rates for years to come trading at a value-type multiple, while aggressively buying back its own stock.

What to Expect in 2019 and Onwards

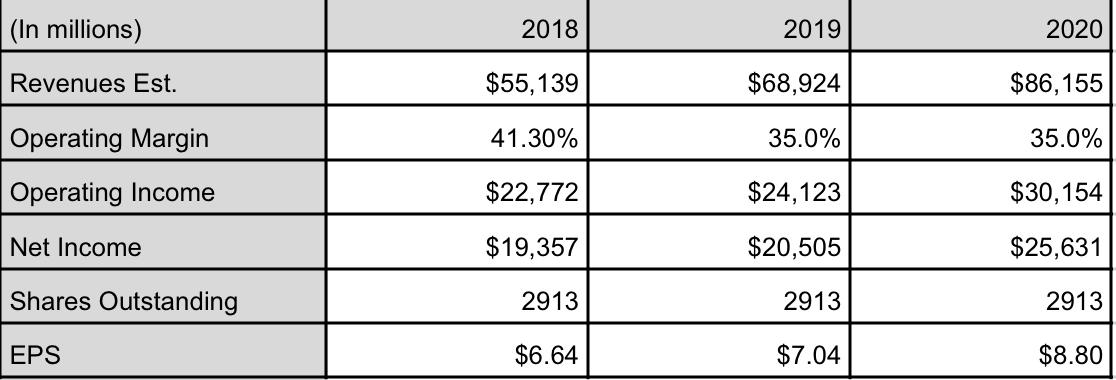

After the last quarter’s results, I need to update my expectations for next year. I did not anticipate margins to drop as quickly towards the 35% range as they did in Q3. For Q4, I am projecting 25% revenue growth and 35% operating margins - both numbers being on the conservative end given management’s guidance. I also am projecting 35% margins immediately in 2019 with 25% revenue growth. Even though revenue growth is expected to pick up following the major changes in 2019, I use the same 25% revenue growth in 2020 as well. I should note that revenues had been growing over 40% prior to the recent struggles.

Below, I show my revenue and earnings expectations for 2019 and 2020:

(Chart by Author)

As we can see above, while I expect EPS growth to be slower in 2019 due to the increased expenses, EPS growth picks up dramatically in 2020, when expenses will no longer grow so rapidly. I also note that these estimates will probably prove to be too low, as I am counting on FB to strongly beat on my operating margin assumptions as well as revenue growth rates. Furthermore, the estimates do not include any effect from share repurchases, which could be a major factor moving forward if FB decides to monetize its cash hoard, or better yet, take some leverage onto its balance sheet.

Valuation

FB is trading at its cheapest levels ever on a historical basis.

Of course, it trades much lower than its 5-year average of 55 times earnings:

(Chart by Author, data from Morningstar)

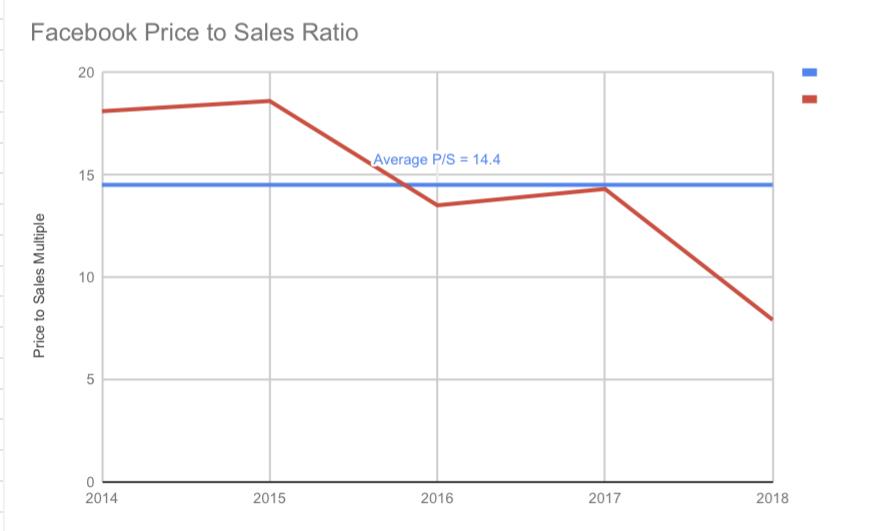

The stock is also trading significantly lower than its 5-year average of 14.4 times sales:

(Chart by Author, data from Morningstar)

Compared to the S&P 500 too, FB appears to be cheap. Whereas the S&P 500 trades at about 22 times trailing earnings, FB trades 20.2 times trailing earnings of $6.64 per share.

Again, I anticipate 2019 to be a year of conservative-to-moderate earnings growth for FB, before accelerating once again in 2020. The company arguably has more consistent and higher-quality earnings than the broader market due to its pristine net cash balance sheet (as compared to the average 1.7 times debt to EBITDA of the S&P 500), secular growth tailwinds of online advertising, and social networking platforms (especially Instagram) gaining more and more momentum due to growing user counts and engagement. I greatly doubt that its growth story has been significantly impaired in the long term. FB arguably deserves a larger premium - now let’s try to determine a price target.

Price Target

My 12-month price target for FB is $200, which would be about 29 times 2019 earnings but 22.7 times 2020 earnings. While it may appear high considering the EPS growth slowdown in 2019, the valuation would appear reasonable once EPS growth picks up again in 2020. This could be reached, for example, through continued strong execution, as well as if management could show surprise upside perhaps through accelerated share repurchases funded by levering up the balance sheet. I should, however, once again stress that this should be viewed as a long-term investment, as the company might not show meaningful EPS growth until 2020.

Risks

The biggest risk is that FB loses its dominance in the online advertising space and sees a larger-than-expected growth slowdown, or even begins to see negative results. This risk cannot be ignored considering that the company currently does not really have revenues other than those from online advertising through its social networking platforms. However, considering that rival Snapchat (SNAP) recently reported struggling user growth, it does not appear that FB has significant competitors that would challenge to take over. That means one would need to count on a widespread move away from the use of social networks for this risk to play out - I find this highly unlikely.

Another risk is that management does not view the company"s shares to be as cheap as your author does, and prefers to let them linger at low levels. This would manifest itself in decelerated share buybacks. However, FB has been very diligent in directing all of its free cash flow towards share repurchases this year, showing that management does view shares as cheap. Furthermore, it is unlikely that the company will willingly risk employee turnover due to the struggling share price, as share-based compensation continues to be a significant component of employee expenses.

Cheap stocks can always get cheaper. I didn’t think that FB would be able to fall below $150, but here we are. I, however, am not afraid of this possibility, because it would only help the company achieve higher EPS numbers due to a more powerful share repurchase program.

Conclusion

It seems that the further FB falls, the more negativity surrounds it. The company, however, continues to execute and buy back as much stock as its free cash flow allows for. Assuming management can deliver on improving data privacy in 2019, company earnings may continue their strong growth rate and prove the skeptics wrong. FB shares have about 50% upside to my price target in the next 12 months.

If you liked this article, please scroll up and click "Follow" next to my name to not miss any of my future articles. I am always looking to expand my network of intelligent investors. I have a reputation for replying to every comment, leave a comment below!

(TipRanks: FB: Buy)

Disclosure: I am/we are long FB.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment